Chelsea's transfer spending since Todd Boehly's Clearlake Capital consortium acquired the club in May 2022 has been unprecedented, but most of the talk has been of how they have only managed to do this via the use of an accounting “trick”, known as player amortisation.

In a previous blog, I explained how this does indeed help Chelsea meet Financial Fair Play targets, but I would now like to focus on two areas:

Place Chelsea's transfer spend into context.

The real cost of their frenetic activity in the transfer market.

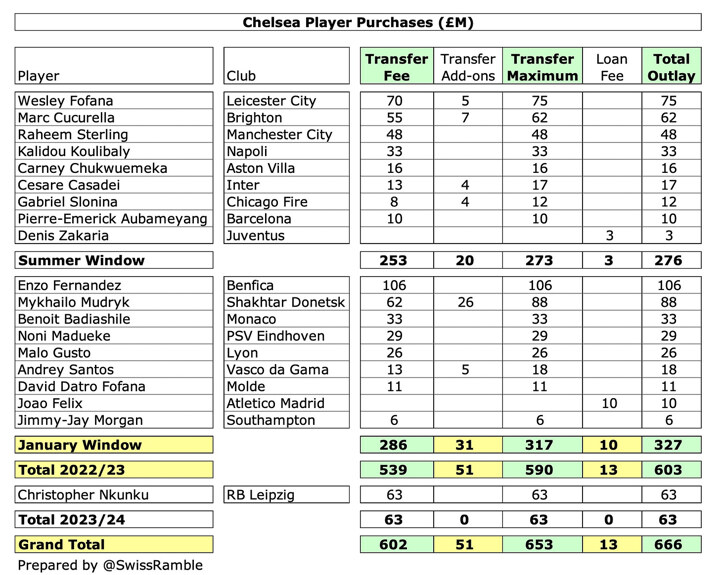

Player Purchases

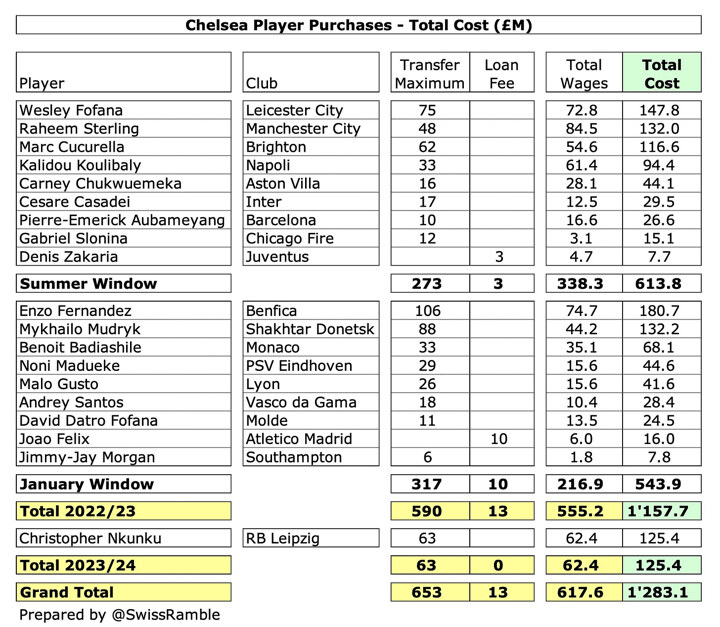

Chelsea ended up spending an incredible £286m in the January transfer window, which takes their total spend for the 2022/23 season to £539m. This included the deadline day acquisition of Enzo Fernandez from Benfica for £106m, which was a new British transfer record, eclipsing the £100m that Manchester City paid to Aston Villa for Jack Grealish.

In addition, Chelsea brought in Mykhailo Mudryk, Benoit Badiashile, Noni Madueke, Malo Gusto, Andrey Santos, David Datro Fofana and Jimmy-Jay Morgan.

In fact, if we include transfer add-ons and the £10m loan fee to secure the services of Joao Felix for six months, the outlay in January was £327m with the expenditure for the full season being £603m. Adding the £63m committed to purchase Christopher Nkunku from RB Leipzig in the summer would give a spooky £666m.

It seems like ages ago now, but only this summer Chelsea spent another quarter of a billion pounds, including the big money buys of Wesley Fofana, Marc Cucurella, Raheem Sterling and Kalidou Koulibaly – many of whom now find themselves on the bench.

Other Clubs' Opinions

Chelsea's spending has puzzled the managers at some of their Premier League rivals.

After spending only £37m on Cody Gakpo in the January window, Liverpool's Jürgen Klopp said, “I don't understand this part of the business, but it's a big number. I don't understand how it's possible, but it's not for me to explain how it works.”

Manchester City spent even less, only £10m on Maximo Perrone from Velez Sarsfield, and Pep Guardiola took the opportunity to have a dig at the media when asked about Chelsea's extravagance, “It's a surprise, because it's not a state club.”

January Transfer Window

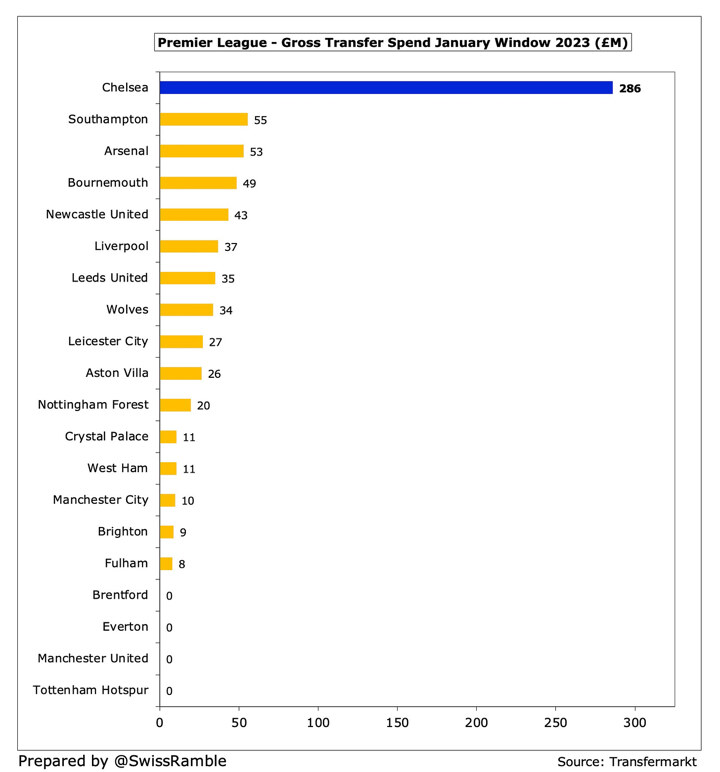

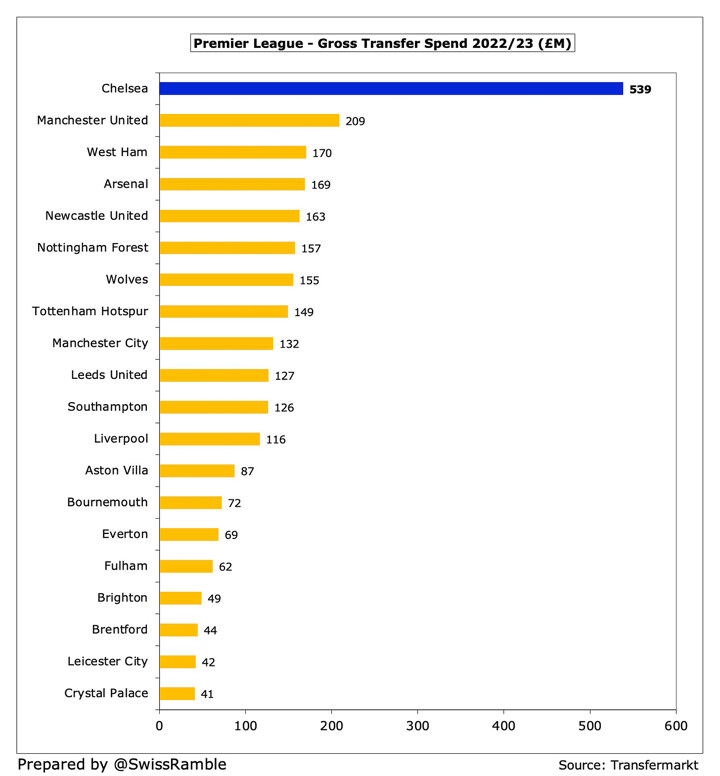

Chelsea's £286m gross transfer spend in the January window was obviously by far the highest in the Premier League, more than five times as much as the closest challengers, Southampton £55m and Arsenal £53m. Four clubs did not spend anything at all: Brentford, Everton, Manchester United and Tottenham (Pedro Porro arrived on loan with obligation to buy).

To place Chelsea's expenditure into perspective, it was £180m more than the rest of the Big Six combined.

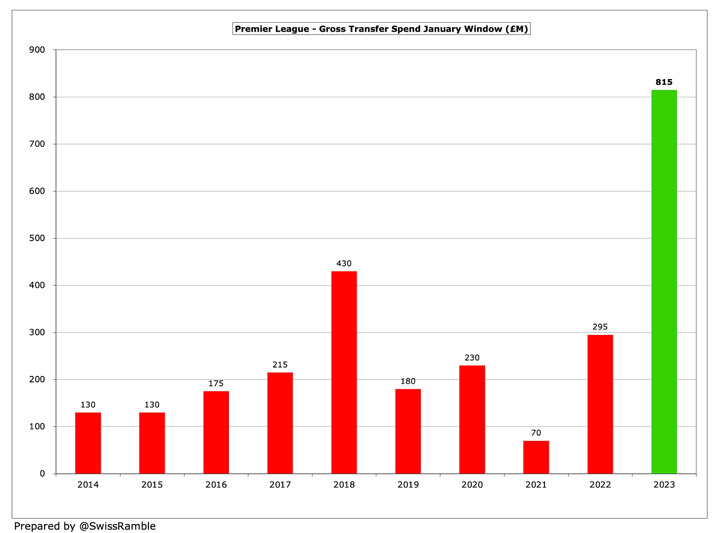

This helped to contribute to the largest ever January window transfer spend in the Premier League of £815m. This is almost twice as much as the previous record of £430m in 2018 and nearly triple the previous season's £295m.

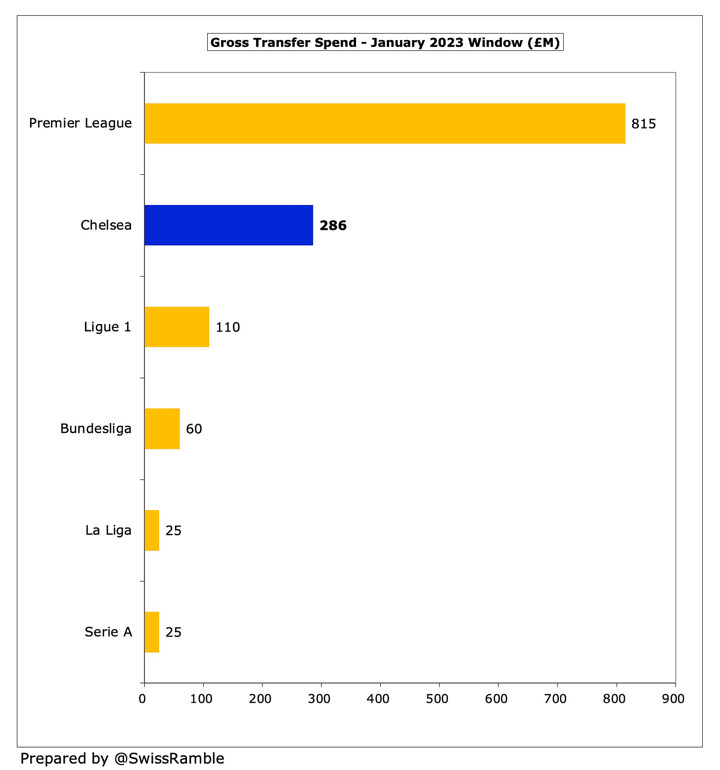

Incredibly, Chelsea on their own spent far more than La Liga, the Bundesliga, Serie A and Ligue 1 put together: £286m for the Blues compared to £220m for the continental leagues. This only underlined the widening financial gap between England's top flight and the rest of Europe.

Chelsea's new owners are clearly in a hurry, as they have attempted to replenish and rejuvenate their squad in a single transfer window, while others clubs would only be capable of doing this over a number of seasons.

La Liga's View

The huge spending in the Premier League led to another broadside from Javier Tebas, the president of La Liga, “The British market is a doped market. You can see it clearly in this winter market, where Chelsea have made almost half of the signings in the Premier League.” In fact, it was around 40%, but you take his point.

Tebas added, “The Premier League is a competition that loses billions of pounds in the last few years. And this is financed with contributions from the owners, in this case large American investors who finance at a loss. This does not happen in the Spanish League and neither does it happen in the German League.”

The key point here is the knock-on effect it has on other leagues: “It is quite dangerous that the markets are doped, inflated, as has been happening in recent years in Europe, because that can jeopardise the sustainability of European football.”

That said, many continental clubs now rely on an annual injection of funds from the Premier League via lucrative player sales. The price they can secure from clubs outside England is clearly lower, e.g. recently Atletico Madrid only paid £3m to Barcelona for Memphis Depay, who would surely have cost an English club much more.

2022/23 Transfer Spend

Chelsea have spent over half a billion pounds (£539m) on transfers in the 2022/23 season, i.e. since Boehly's consortium arrived – and this excludes add-on fees and loan signings. Their maximum outlay is north of £600m.

Chelsea's purchases “only” accounts for 20% of the Premier League's gross transfer spend over the season, as many clubs largely did their business over the summer, including Manchester United £209m and West Ham £170m.

Liverpool fans will be unhappy about the relatively low level of spending at Anfield, as their £116m was only 12th highest in the Premier League, behind the likes of Nottingham Forest £157m, Wolves £155m, Leeds United £127m and Southampton £126m.

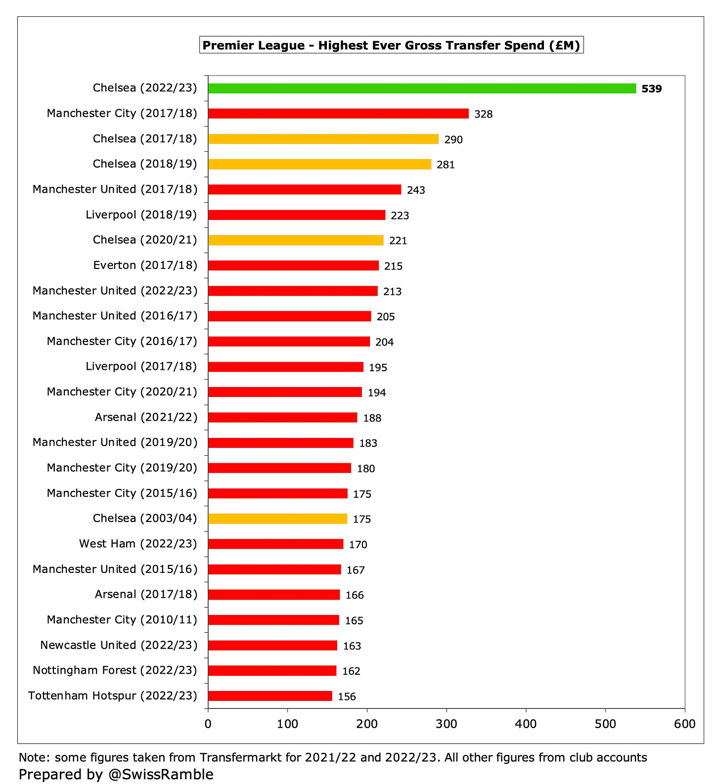

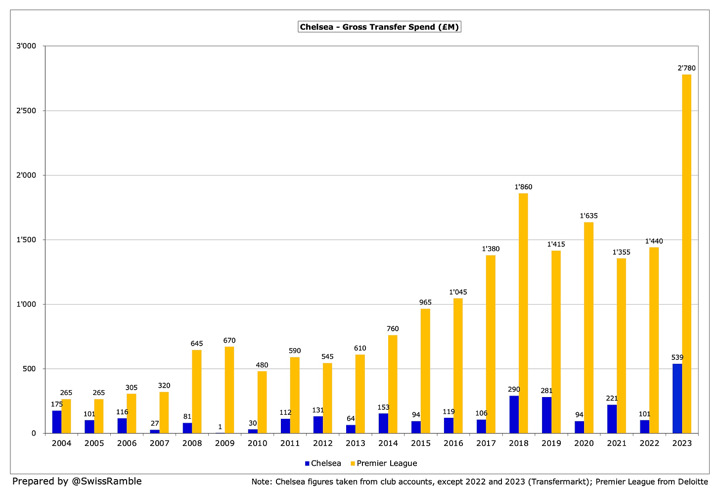

Chelsea's gross spend this season is easily an all-time high for the Premier League, almost £200m more than Manchester City's £328m in 2017/18. Of course, Chelsea are no strangers to splashing the cash, being responsible for three of the top four annual transfer outlays (and four of the top seven) in PL history.

Transfer Trends

When the consortium led by Boehly and Clearlake Capital purchased Chelsea, not many people would have expected them to be so active in the transfer market, given that private equity investors usually have a laser-like focus on the return on capital.

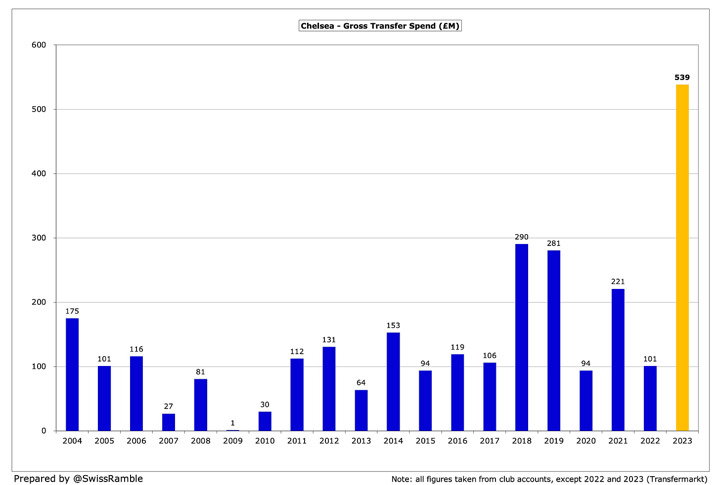

Therefore, it is somewhat surprising that the 2022/23 season has seen Chelsea's highest ever gross transfer spend. The £539m outlay (excluding potential add-ons) is significantly more than the largest outlay under Roman Abramovich, which was £290m in 2017/18.

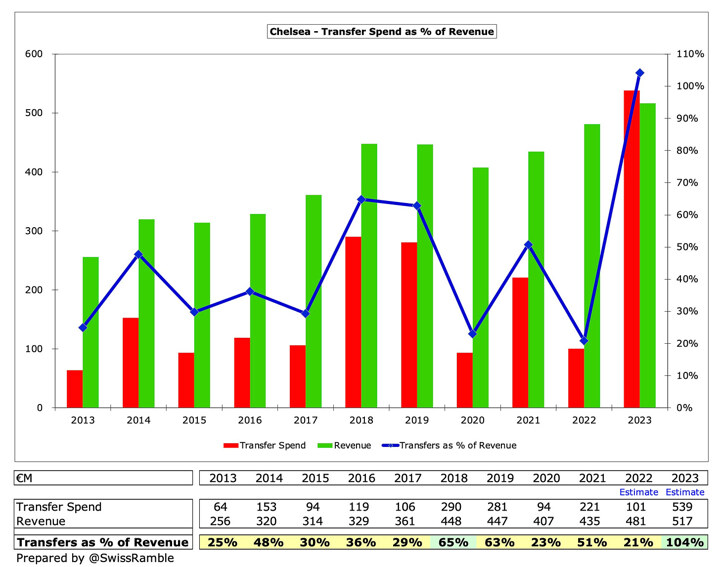

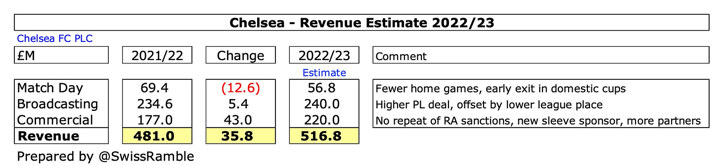

As a result, Chelsea have spent more on transfers this season than their (projected) annual revenue, as the £539m outlay is 104% of £517m revenue. Even under Abramovich, this ratio was much lower with the previous highest being 65% in 2018.

Furthermore, the 2022/23 revenue estimate of £517m is fairly generous, assuming a 7% increase from last season's £481m, driven by commercial growth.

In fairness, Chelsea are not alone in being more active in the transfer market, as the Premier League established a new record high of £2.8 bln in 2022/23. This was almost a billion more than the previous peak of £1.9 bln in 2018 and nearly twice as much as prior season's £1.4 bln.

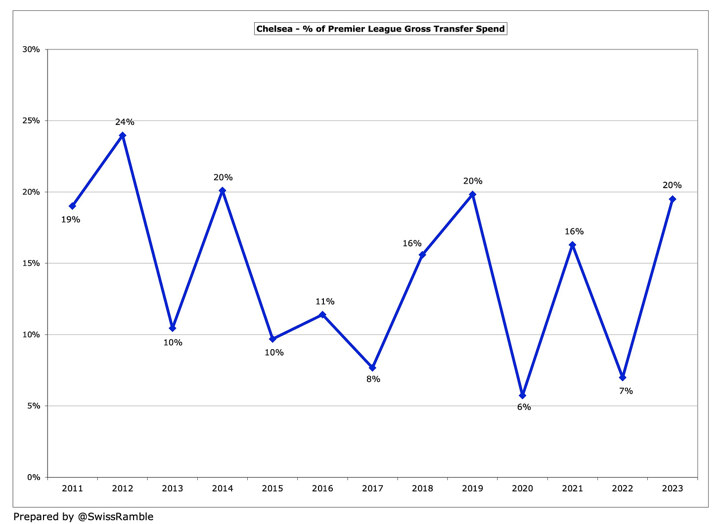

Chelsea were obviously the main driver of this growth, accounting for 20% of total Premier League gross transfer spend. This is higher than normal, but is by no means out of the ordinary for the Blues, who have achieved similar levels on three other occasions since 2012.

How can they do it?

Many people, especially supporters of other clubs, are asking how Chelsea can spend so much, but there are actually two questions here:

Does the club have enough money?

How can Chelsea still be in line with Financial Fair Play regulations?

Does the club have enough money?

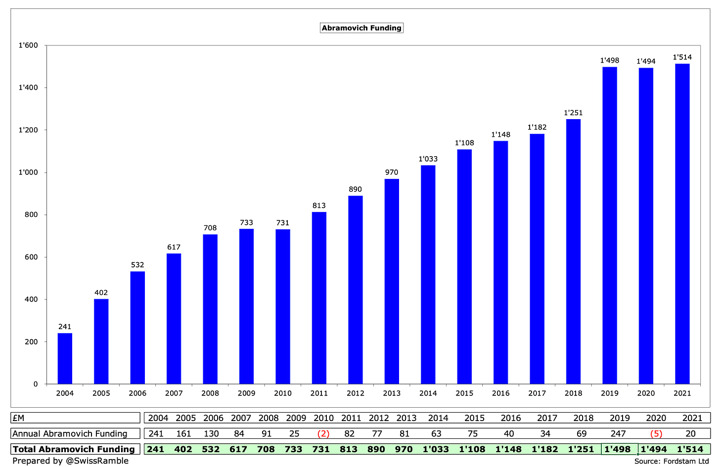

Roman Abramovich regularly provided cash injections to Chelsea during his tenure, putting in over £1.5 bln, resulting in the highest debt in the Premier League. However, the good news for the Blues is that the former owner has reportedly written-off this balance as part of the club sale, though it is not yet clear whether this was via a repayment waiver or conversion into equity.

The new owners also have plenty of cash, given they paid a princely £2.5 bln to acquire the club, while committing to a further £1.75 bln of infrastructure investment.

In any case, like all other football clubs, they will be paying off transfer fees in instalments, so they don't have to find the funds all at once.

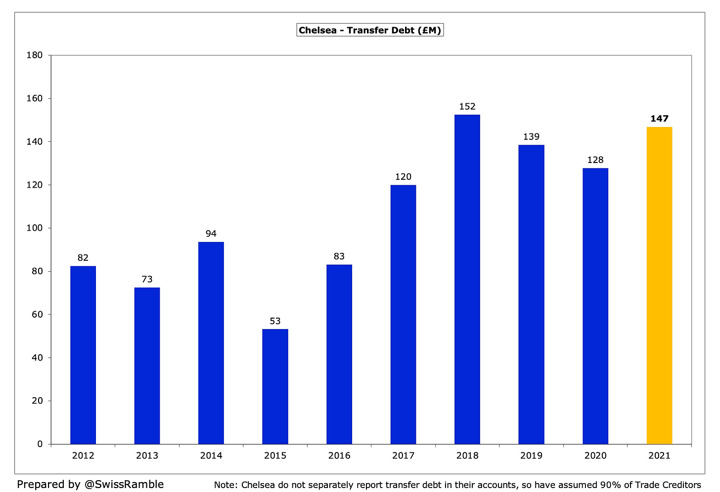

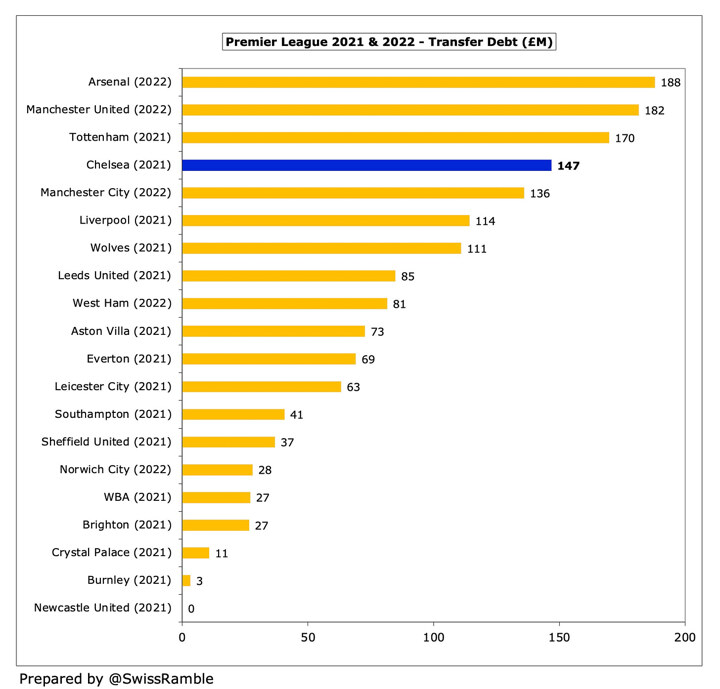

Chelsea's transfer debt has increased over the past few years to £147m in 2021, but this was still a fair bit lower than other elite clubs, e.g. Arsenal owed £188m as of June 2022, while Manchester United's payables surged to a Premier League record of £307m in Q1 2022/23.

How can Chelsea still be in line with FFP regulations?

This is where we need to look at how player trading is reported in a club's accounts, as this has greatly helped Chelsea's ability to stay within FFP regulations.

Player Trading Accounting – Purchases

The key point here is that when a player is purchased the cost is spread over a few years, but any profit made from selling a player is booked to the accounts immediately.

Transfer fees are not fully expensed when a player is purchased, but are written-off evenly over the length of the contract via player amortisation. So if a player is purchased for £60m on a 5-year contract, the annual amortisation would be £12m, i.e. £60m divided by 5 years.

This is a completely normal, standard accounting treatment. The only “innovative” step that Chelsea have taken is to sign players on long contracts, which means that the cost of the transfer fee is spread over more years. This results in a lower annual charge being booked to the accounts, but the bill will still have to be paid someday. So this is not exactly the “silver bullet” that some have claimed.

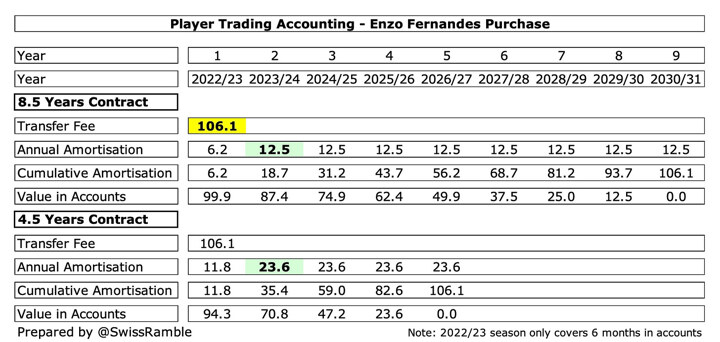

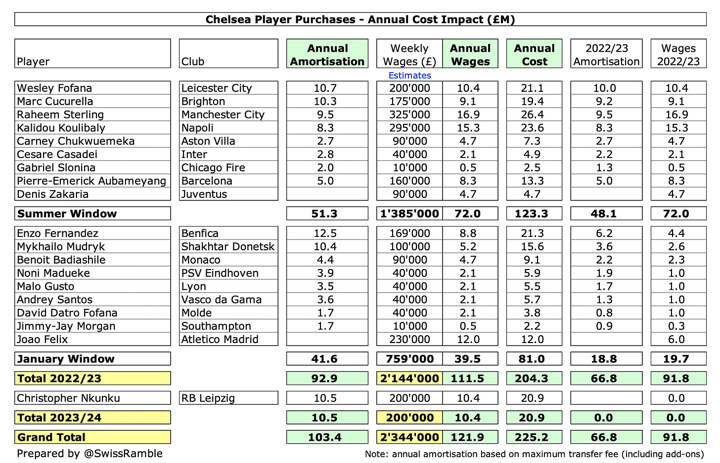

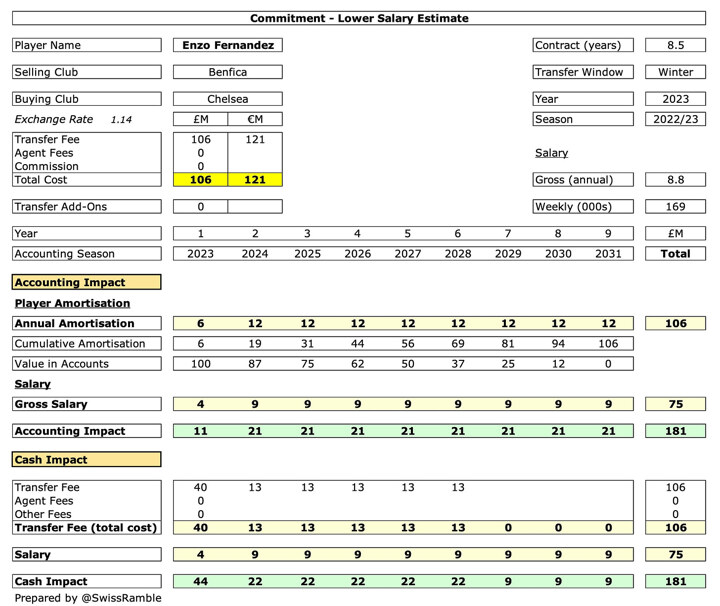

However, in the short term, it does help the books look better, as we can see with Enzo Fernandez. He was bought for £106m on an 8½-year deal, which works out at £12.5m annual amortisation. If he had signed on a more normal 4½-year contract, the annual amortisation would have been nearly twice as much at £23.6m.

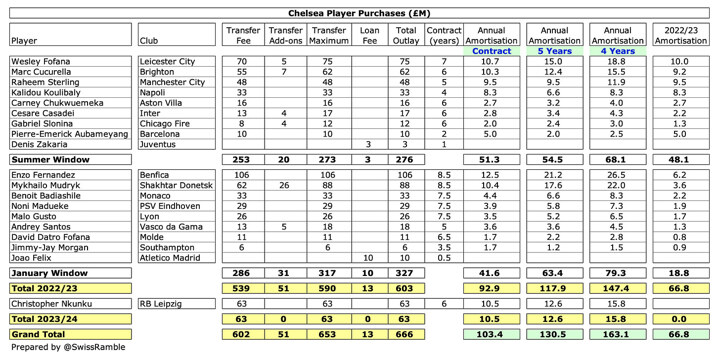

Many of the other arrivals have also been on very long contracts. Mudryk put pen to paper for 8½ years, while Badiashile, Madueke and Gusto signed for 7½ years, and Wesley Fofana for 7 years.

Looking at Chelsea's player purchases in 2022/23, we can see the difference between the long-term contracts and more normal length contracts. The annual amortisation on the actual contracts is £103m, but this would increase to £131m on 5-year contracts and £163m on 4-year contracts.

The amortisation impact in 2022/23 is lower at £67m, as the January signings will only have six months' booked to the accounts (and will almost certainly exclude add-ons).

In a classic case of shutting the stable door after the horse has bolted, UEFA has now clamped down on the amortisation “trick” by setting a maximum 5-year contract length for the FFP calculation, regardless of how long a player signs for. The new rule will only be implemented this summer, and not applied retrospectively, so the treatment of Chelsea's signings will not be impacted.

Player Trading Accounting – Sales

Let's look at how player sales are booked, using a few recent Chelsea examples that highlight the difference between the more favourable accounting treatment and the real world.

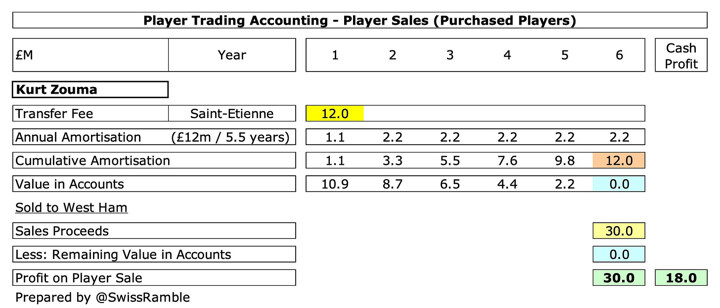

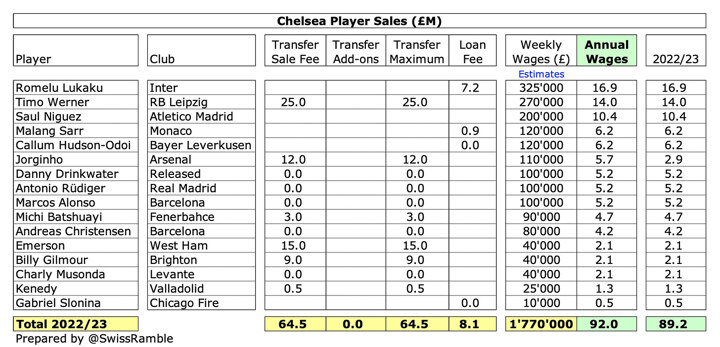

First, Kurt Zouma was sold to West Ham for £30m, having been bought from Saint Etienne for £12m, leading to a cash profit of £18m. However, as his original transfer fee had been fully amortised in the accounts, the club could book a much higher £30m profit.

Better still, Davide Zappacosta was bought from Torino for £22.5m on a 4-year contract and sold to Atalanta four years later for only £8m, leading to a £14.5m cash loss. However, thanks to the “wonders” of accounting, this would actually be shown as an £8m profit in the books, as the Italian full-back had again been fully amortised.

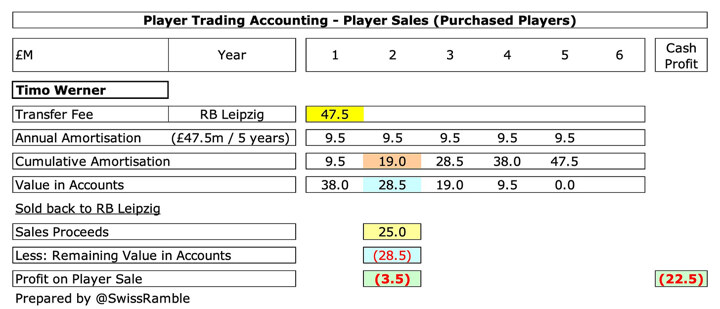

The accounting treatment has boosted the finances even in the case of the misfiring Tino Werner, who was sold back to RB Leipzig after just two seasons at a £22.5m loss (purchase £47.5m, sale £25m). However, as the club had already booked two years of amortisation amounting to £19.0m, his remaining value in the accounts was only £28.5m, so the reported loss was much lower at just £3.5m.

Academy Products

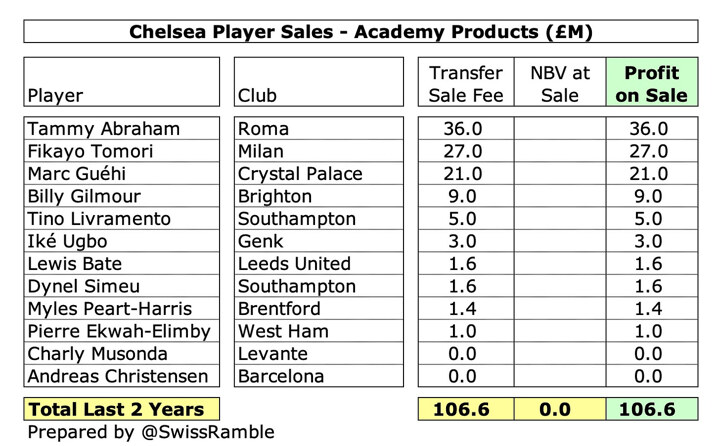

That's great, but, hold on a moment, it actually gets even better, as players developed in a club's academy have no cost in the accounts. There is only a cost if a club has paid to secure a player's registration from another club. This means that any sale of an Academy product produces pure profit.

This has been of particular importance to Chelsea and helps explain why they have hoarded young talent, keeping players on the books, even after numerous loans elsewhere.

In this way, the Blues have booked more than £100m from the sale of Academy players in the last two years, earning big money from the transfers of Tammy Abraham to Roma, Fikayo Tomori to Milan, Marc Guéhi to Crystal Palace and Billy Gilmour to Brighton.

In the future, Chelsea could look to replicate this success, as there are many players that are likely to be sidelined by the new arrivals, but would still raise good money, including Conor Gallagher, Ruben Loftus-Cheek, Trevor Chalaboah, Callum Hudson-Odoi, Levi Colwill and potentially even Mason Mount.

Business Model

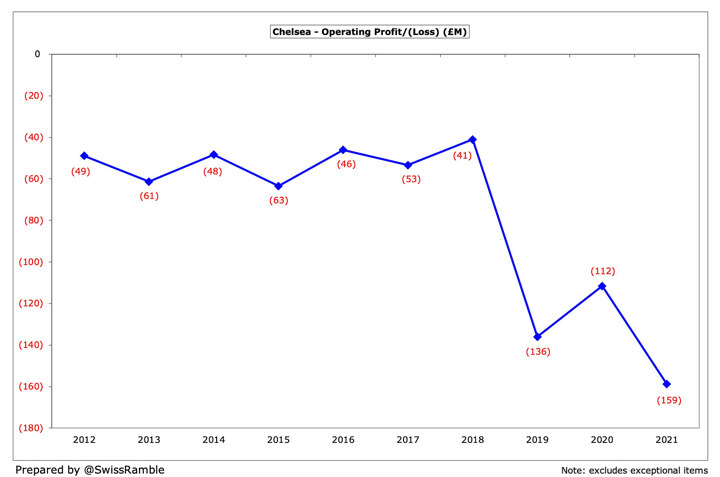

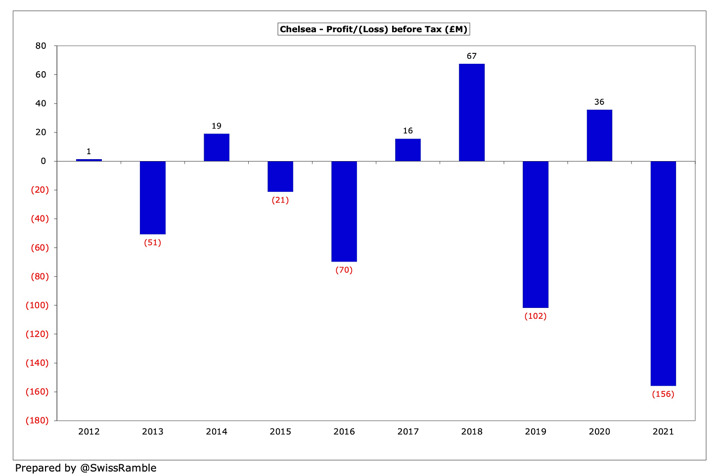

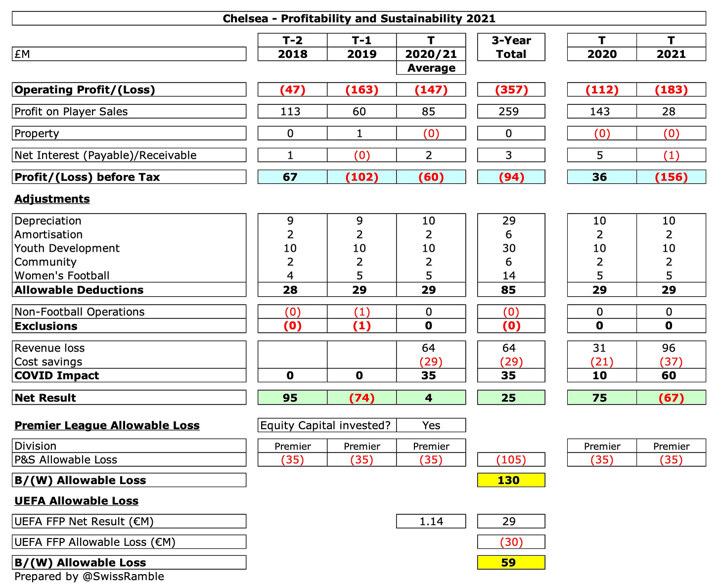

Chelsea's business model over the past few years owes a great deal to the accounting treatment for player trading, as it has essentially been to offset large operating losses with profits from player sales.

In the 10 years up to 2021, Chelsea have consistently posted large operating losses, adding up to more than three-quarters of a billion pounds (excluding another £110m of exceptional items).

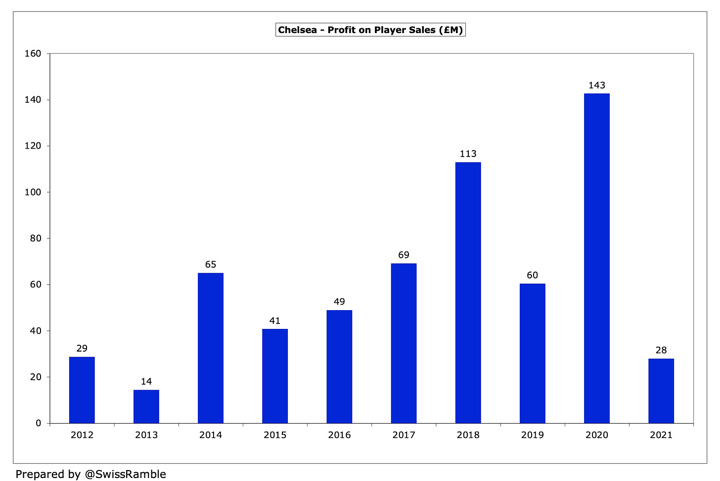

However, these losses have been largely offset by a very impressive £611m profit from player sales in the same period, including two seasons above £100m.

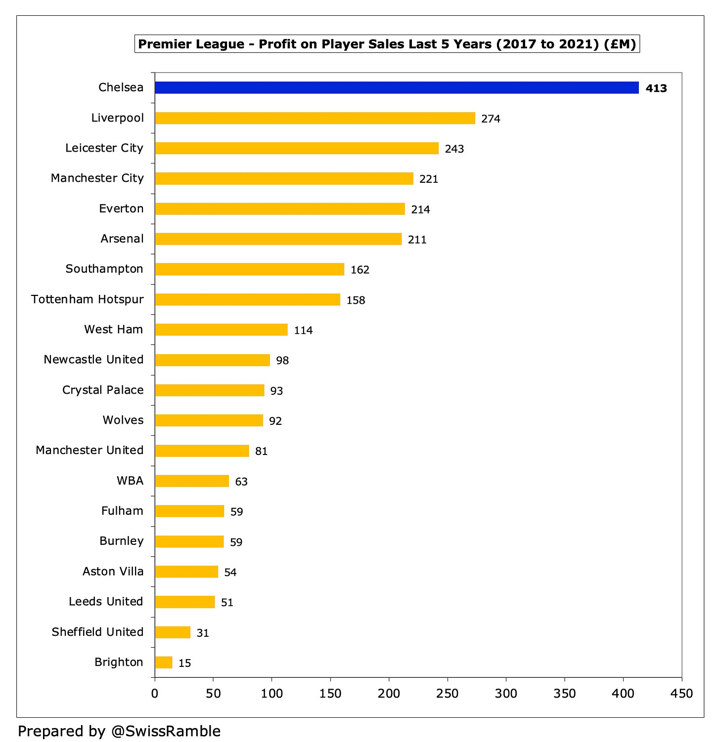

Indeed, in the last five years alone, they generated a staggering £413m profit, which is around 50% more than the next highest club in the Premier League, namely Liverpool with £274m.

Chelsea's approach is perhaps best illustrated by the 2019/20 season, when their £112m operating loss was more than compensated by £143m profit from player sales, leading to a net £36m profit.

That said, Chelsea still reported net losses in half of the last 10 years, so player trading is not a total panacea, but it sure helps to limit the damage. The bottom line is that if Chelsea can continue to sell well, then they should be fine in terms of financial fair play.

Accounting Impact of Player Purchases

With the usual caveats about estimates being used for wages and transfer fees, I reckon that Chelsea's player purchases this season will increase the annual cost base in the accounts by £225m, i.e. not far off an incredible quarter of a billion. This is split between £122m wages and £103m player amortisation.

The impact on the 2022/23 accounts will be smaller at around £159m, as the January signings will only cover six months this season (wages £92m, player amortisation £67m).

Player Amortisation

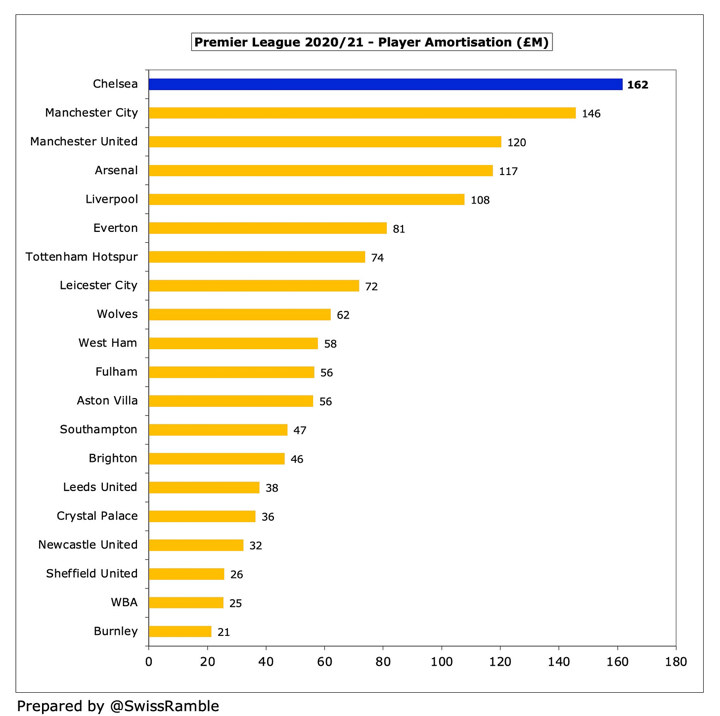

Chelsea's £162m player amortisation was already the highest in the Premier League in 2021, a fair way above Manchester United £149m and Manchester City £141m, reflecting the club's substantial transfer expenditure.

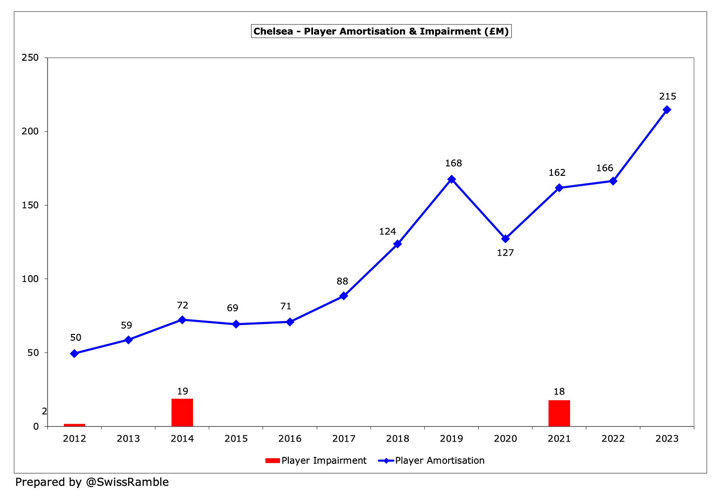

Chelsea booked £12m player impairment in 2020/21, which will help reduce amortisation going forward, while there should also be a reduction from some contracts being fully amortised or extended.

Nevertheless, based on my transfers model, player amortisation should still increase to £166m in 2021/22 and to a hefty £215m in 2022/23. It will be even higher the following season, due to the full-year effect of January signings.

The player amortisation would be off the charts if the club had signed players with a more standard contract length.

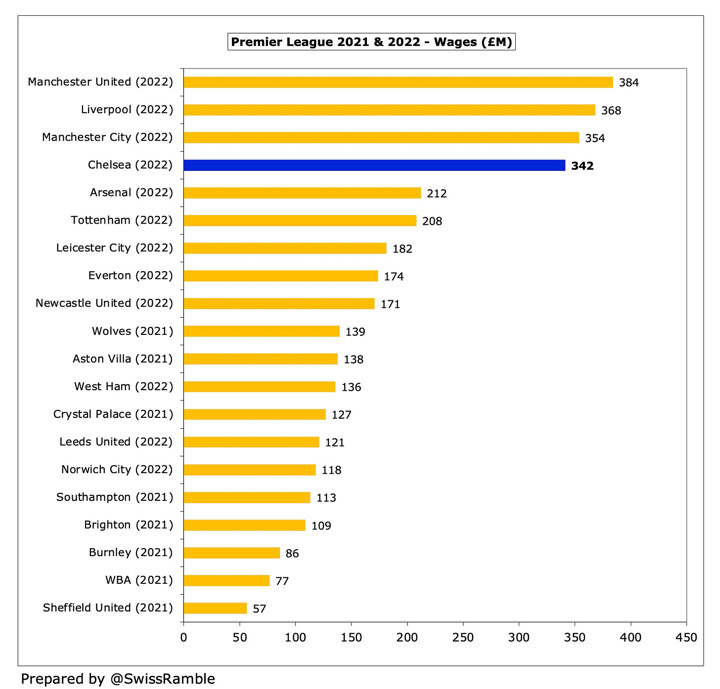

Chelsea's £342m wage bill is currently the fourth highest in the Premier League, only surpassed by Manchester United £384m, Liverpool £368m and Manchester City £354m.

The club has not yet published accounts for the 2021/22 season, but Chelsea's wages can be calculated based on the revenue (£481m) and wages to turnover ratio (71%) included in Deloitte's Money League.

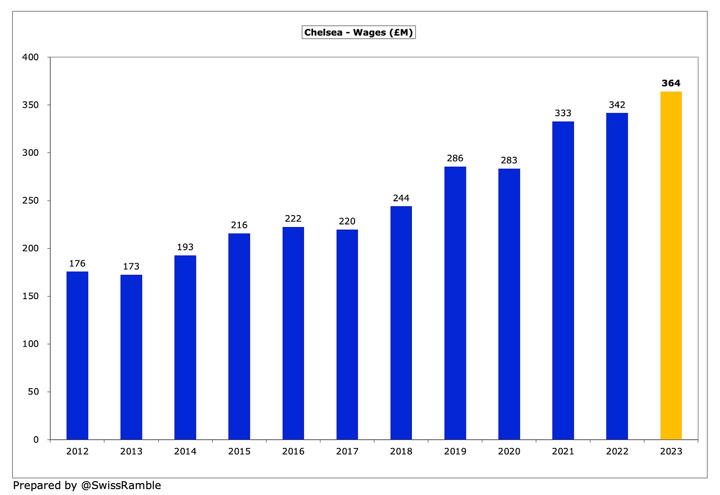

Taking the £342m as the new base, I have added a £3m increase for the net impact of transfers in 2022/23 plus another £20m for contract extensions, giving a £364m wage bill.

Some might be surprised that the net impact on wages of 2022/23 transfers is only £3m, but the £92m increase from player purchases has been largely offset by an £89m reduction to player sales (and loans).

It's not always appreciated that even when a player is sold for very little or even leaves on a free transfer, there is still a benefit in terms of savings in the wage bill. Similarly, if you can persuade the other club to cover all or part of a player's wages, then a loan can also help the finances.

Financial Fair Play

I don't intend to go into all of the minutiae of FFP, as I covered this in painstaking detail in a recent blog.

However, I would point out that clubs are given a lot of assistance in meeting targets, as they can improve the reported financials in a number of ways:

Deductions for “healthy” expenditure (depreciation, non-player amortisation, youth development, women's football and community).

Adjustments for adverse COVID impact.

Assessed over a 3-year monitoring period, so two years of losses can be compensated by one profitable year.

Most importantly, they don't actually have to break-even, as the allowable loss over three years in the Premier League is a chunky £105m (£35m a year).

UEFA's allowable losses are tighter, but from 2023/24 the limit for the 3-year monitoring period has doubled from €30m to €60m and can be further increased to €90m if the club is deemed to be in good financial health.

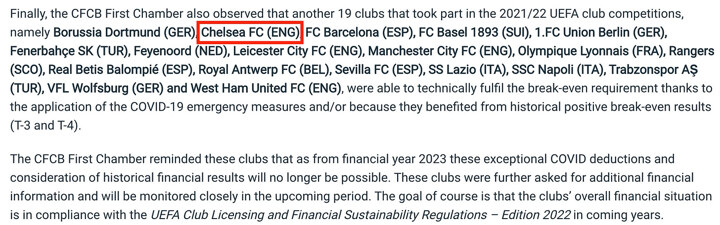

In fact, Chelsea are already on UEFA's watchlist, along with another 18 clubs (including Manchester City, West Ham and Leicester City), as they only met the break-even requirement “thanks to the application of the COVID-19 emergency measures and/or because they benefited from historical positive break-even results.”

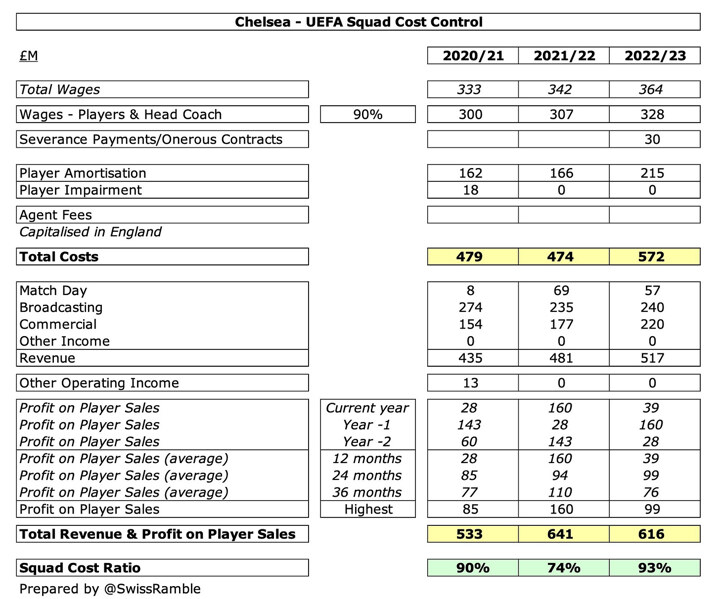

Squad Cost Control Ratio

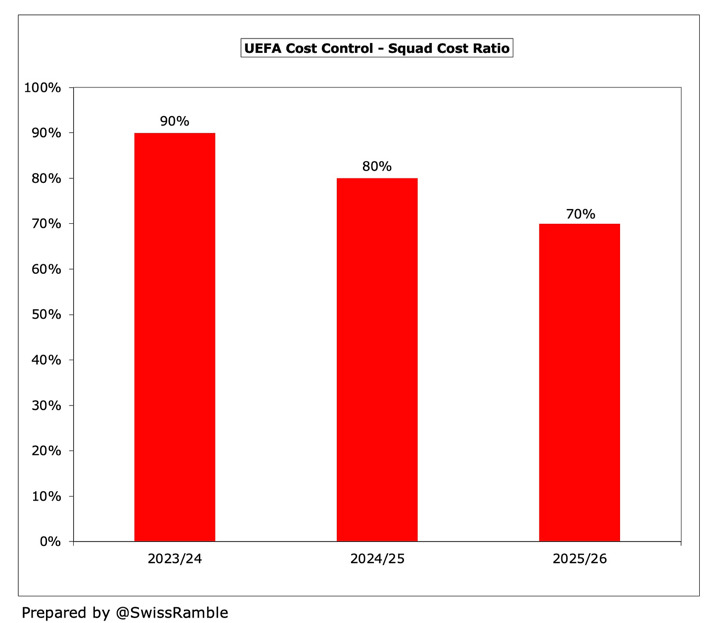

UEFA have also introduced squad cost control via a new ratio of player wages, transfers & agent fees that will be limited to 70% of revenue & profit on player sales, though there will be a gradual implementation over 3 seasons (90% in 2023/24, 80% in 2024/25 and 70% from 2025/26), giving clubs time to get their house in order.

It is worth noting that the cost ratio does not include all wages, only those for players (male professionals) and the head coach, but it does also include bonuses, image rights and termination payments. Based on a review of a few clubs, around 90% of total wages go on players.

Transfer fees are assessed in the cost control ratio via player amortisation (and impairment). Note: agent fees are capitalised, so they are included in the amortisation figures.

The most important element of the denominator in the cost control ratio is obviously the revenue reported in the accounts.

However, the calculation also includes profit on player sales, which will be assessed over 36 months, pro-rated to 12 months. Note: in the introductory period, this will be “the better of 12, 24 or 36 months”, so Chelsea would once again be boosted by their profitable player trading.

Using these criteria, I estimate that Chelsea's ratio would be around 93% for 2022/23, so “there or thereabouts” in terms of the initial 90% target for the introduction in 2023/24. Of course, they would then have to rapidly improve matters, as the target will drop to 70% in 2025/26.

It has also been reported that Chelsea will try to adjust their FFP submissions for revenue lost during the three months last year when the club was impacted by the sanctions imposed by the government on former owner, Roman Abramovich, which included no further ticket sales and the closure of the club shop.

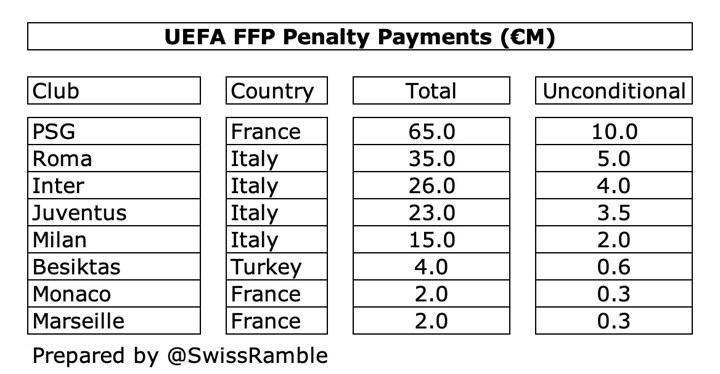

Finally, Chelsea are unlikely to be too concerned if they end up a little above the allowable loss. Looking at the most recent UEFA penalties announced in September 2022, the payments were not too onerous for a club with Chelsea's financial backing.

Even when the fine was as much as €65m (for Paris Saint-Germain), only a small amount of the settlement was paid immediately (€10m) with the remaining €55m conditional. This will depend on future compliance with targets and Chelsea's board would be confident of delivering better figures in the future.

Boehly's consortium might consider such a penalty to effectively be a cost of doing business and worth paying if it allows them to build a squad capable of challenging at the highest levels.

Reality Bites

OK, that's enough about how the fancy financial footwork of the bean counters can help avoid any issues with FFP, but what does Chelsea's spending mean back in the real world?

The fact is that however a club records the transactions in the accounts, the bills still have to be paid. All that happens with longer contracts is you push the day of reckoning further down the road, while your total cost/commitment is obviously higher with a longer contract.

In other words, short-term gain, but long-term pain.

Let's take another look at the Enzo Fernandez signing. Some journalists have reported that he will earn €10m a year, which is equivalent to £8.8m (or £169k a week). That would mean £75m wages over his 8½-year deal. Added to the £106m transfer fee, that would give a total commitment of £181m.

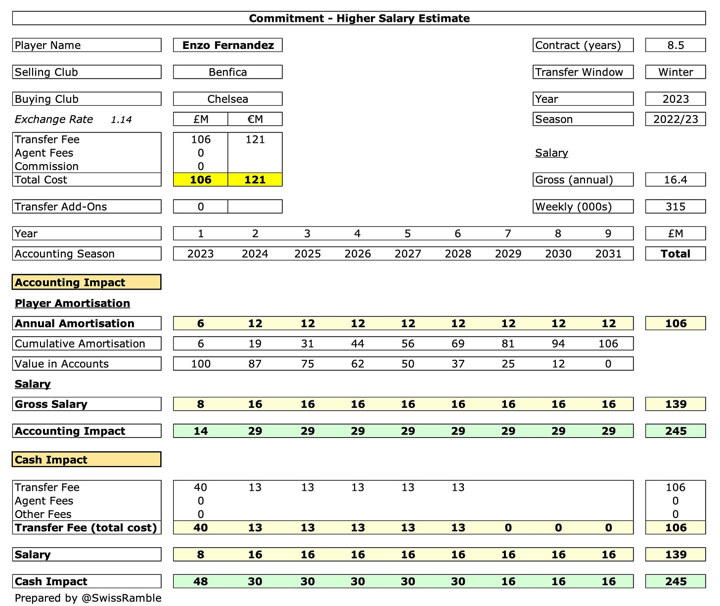

Of course, his salary is not a matter of public record, so this is only an estimate. Indeed, some of the football salary websites have Fernandez's wages as high as £315k a week.

If that number is correct, then the wages over the length of his contract would be £139m, taking Chelsea's total commitment to staggering £245m. Although he is clearly a very talented player (and a World Cup winner), nearly a quarter of a billion pounds is a lot to bet on one individual.

In total, I estimate that Chelsea's signings this season have committed the club to around £1.3 bln, due to a combination of the high spend and lengthy contracts. That is an expensive gamble – unless the players deliver on the pitch.

These figures also exclude agents' fees. If we assume 10%, that would mean another £128m, giving a total cost of £1.4 bln. At 15%, we would be talking about £1.5 bln.

Let's just say that again, because this isn't Monopoly money. In just nine months Boehly and friends have committed Chelsea to spending around ONE AND A HALF BILLION POUNDS.

Furthermore, it is more than likely that wages will increase over these lengthy contracts, either because uplifts have already been built in or players will push for a pay rise if they continue to progress, so the total cost will probably be even higher (if the players stay at Chelsea).

Potential

That said, all of Chelsea's signings in the January window are aged 22 or under, so there is a lot of potential there. The club will hope that they continue to develop, so further appreciate in value, despite some of the high prices paid.

If they do want to sell a player, the theory is that they would be able to secure a good price, as it will be a very long time before the contract runs down.

In addition, if the club anticipates wage inflation, then it makes sense to lock down the players at current wages, rather than give raises as (shorter) contracts approach their end date.

However, the other side of the coin is the many risks associated with this strategy.

Some players will be unhappy at not being picked for the first team (or even the match day squad). As Gary Neville said after last Friday's match against Fulham, “He has to hold that dressing room together, because there's going to be some very upset, disappointed and dejected characters.”

Based on all previous evidence, the odds are that not all of Chelsea's new signings will be successes, so what happens to the flops? It will be far from straightforward to find another club to take such players off Chelsea's hands at a similar level of wages.

Even worse, the underperforming player might just sit there, happy to be trousering the cash, taking up a valuable place in the squad. Chelsea fans will be all too familiar with the Winston Bogarde story.

That might be ancient history, but you only have to look at what has happened to some of last summer's signings, who have seemingly already fallen out of favour, such as Aubameyang and Koulibaly.

Indeed, Auba is a victim of UEFA's regulation that a club can only register three new players in the squad for the Champions League knockout stages. This sort of dilemma is a sign of things to come in terms of squad management.

Given that it is common knowledge that Chelsea now have too many players, other clubs will surely take the opportunity to try to buy on the cheap. Indeed, Chelsea may have to pay up some contracts to encourage the departures of players that are no longer needed.

Importance of the Champions League

One of the key reasons for Chelsea's major investment is to improve their chances of qualifying for the Champions League. This will be a big ask this season, as they currently sit in 9th place in the Premier League, a full 10 points behind the top four.

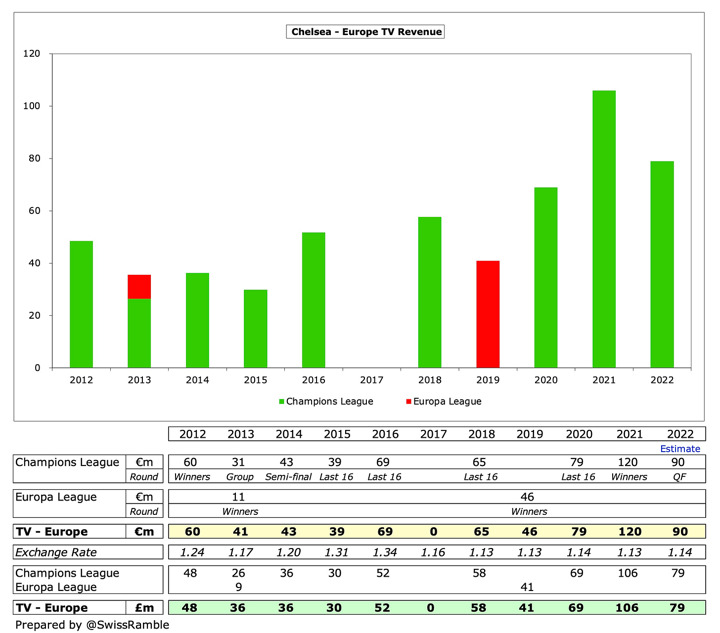

Europe has been an important contributor towards Chelsea's revenue, especially 2020 when they earned £106m by defeating Manchester City to win the Champions League.

Furthermore, that number excludes additional income from gate receipts and bonus clauses in sponsorships and other commercial deals, so a lot of money is at stake.

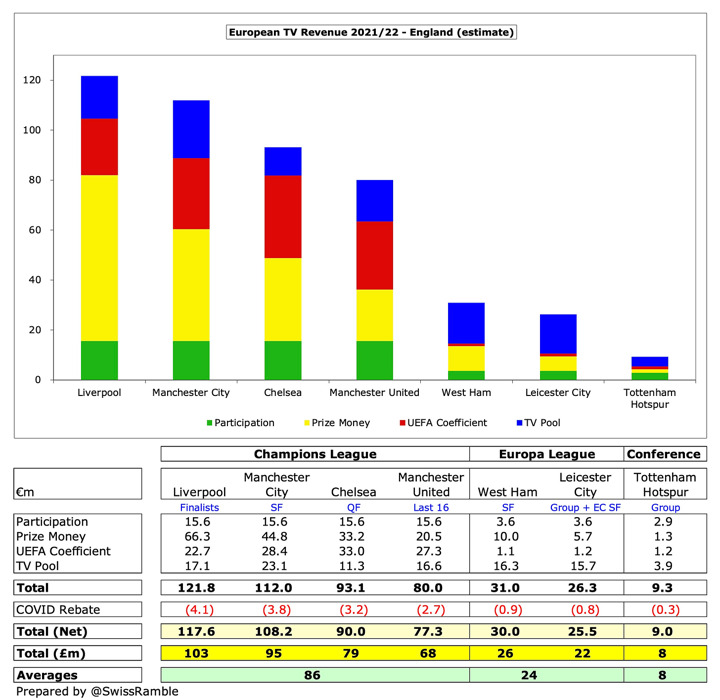

The difference between the earnings in UEFA's three competitions is stark. In 2021/22 England's Champions League representatives received an average of £86m TV money, compared to only £24m in the Europa League and just £8m in the Europa Conference League.

Of course, wages would be reduced if Champions League bonuses did not have to be paid, but the net impact to the bottom line would still be hugely detrimental.

In short, if Chelsea fail to qualify for the Champions league, this would make it very difficult for them to make their FFP calculations add up.

Clearlake Capital

Actually, there is another question that needs to be asked when the dust clears, which is how will Clearlake Capital, Chelsea's owners, make a return on their investment?

As a rule, private equity firms are not known for their willingness to splash the cash, but often look to make efficiencies and cut costs. It will be intriguing to see whether Boehly and co have a cunning plan to boost revenue (and profits).

Frankly, it's not completely clear what their strategy is at the moment. Perhaps this is why they are billionaires – and I'm not.

Conclusion

While it has long been evident that talent acquisition is a core part of the leading clubs' strategies, Chelsea have pushed this to the max this season.

In fairness to Boehly, he is at least living up to the promise made when his consortium bought Chelsea: “We're all in – 100% – every minute of every match. Our vision as owners is clear: we want to make the fans proud.”

He added, “Along with our commitment to developing the youth squad and acquiring the best talent, our plan of action is to invest in the club for the long-term and build on Chelsea's remarkable history of success.”

Boehly might have bet the farm on new players, but he is clearly a man of his word. It's not clear whether his gamble will succeed, but to paraphrase the Sex Pistols, we can safely say, “He means it, man.”

Thanks for reading The Swiss Ramble! Subscribe for free to receive new posts and support my work.